साझा अर्थ संवाददाता

१८ असार २०८३, बिहिवार

साझा अर्थ संवाददाता

१८ असार २०८३, बिहिवार

Kathmandu, 2nd July: In Nepal’s stock market, optimism often arrives before evidence. A few green screens are enough to change the mood. Screenshots begin to circulate. Facebook groups wake up. YouTube thumbnails become louder.

Investors who were silent during the fall return with confidence. Someone says the market has turned. Someone says big players are entering. Someone says regulatory reform is coming. Someone says this is the beginning.

For many ordinary investors, it is not just a market movement. It is hope.

That is exactly why it can become dangerous.

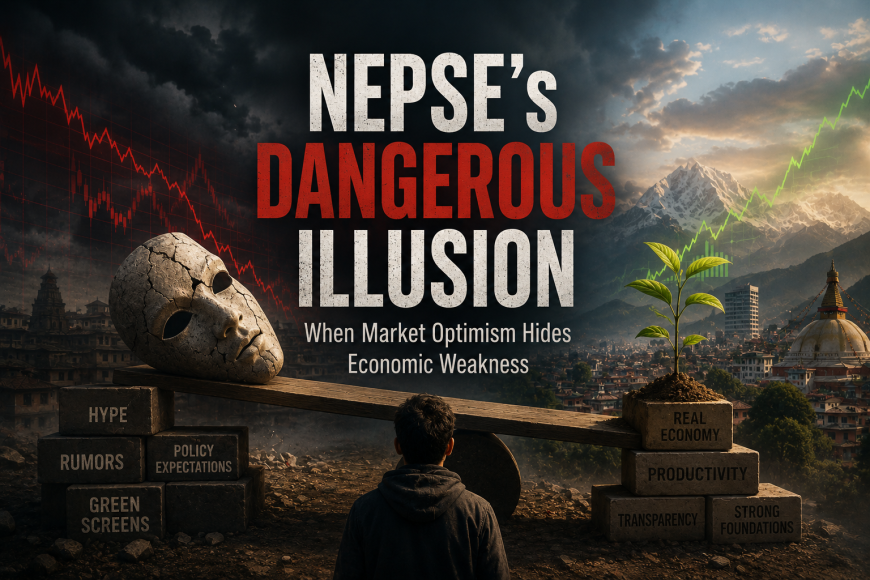

The real problem NEPSE is facing is not simply that the index rises or falls. Markets are supposed to move. Prices respond to expectations, liquidity, fear, greed, earnings, policy, and sometimes pure emotion. The deeper problem is that NEPSE has developed a culture where hope can quickly become certainty, where policy expectation is mistaken for reform, and where a green screen is treated as proof that the economy underneath it is healing.

But a market can turn green even when the economy remains weak.

That is the illusion.

The early-July movement in NEPSE should be understood in that context. On July 1, 2026, NEPSE rose by 44.59 points, or 1.70 percent, to close at 2,652.93, with turnover of Rs 3.856 billion. It was a visible rebound after several days of weakness, but it should not be carelessly called a rally. Two green days do not make a recovery. They only show how quickly sentiment can return when investors are searching for a reason to believe again.

The more important question is not whether NEPSE went up today.

The more important question is: what is it rising on?

If the answer is stronger earnings, productive investment, better regulation, healthier liquidity, and a more confident economy, optimism has a foundation. But if the answer is social media excitement, policy hope, fatigue after a fall, and belief that someone powerful will “save” the market, then investors are not witnessing recovery. They are witnessing confidence being performed.

For many Nepalis, NEPSE is no longer just a stock exchange. It has become a daily emotional event.

People check the index between office work, classes, shop hours, and bus rides. A small investor may own a few IPO shares, a hydropower stock, a bank stock, and a finance company he barely understands. A young investor outside the Valley may follow the market through Facebook posts and short videos. A migrant worker abroad may track NEPSE at night, hoping the money sent home is doing more than sitting in a bank account. A student may know more about bonus shares than about the company’s cash flow.

This is the new NEPSE culture.

In one way, it is positive. The market has brought financial language into ordinary households. Demat accounts, IPO applications, Mero Share, online trading, and secondary-market access have made capital markets more visible than before. More Nepalis now talk about investing, ownership, dividends, and companies.

But access without understanding can become a trap.

The danger is not that ordinary people entered the market. The danger is that many entered a market where noise is often louder than knowledge. For a first-generation investor, the difference between analysis and entertainment is not always clear. A confident social media post can sound like research. A viral chart can feel like proof. A rumor repeated by enough people can start to look like information.

That is how the illusion spreads.

NEPSE is now traded emotionally before it is traded financially.

Every market movement enters a digital machine. A small gain becomes “bull incoming.” A policy rumor becomes “major reform.” A new appointment becomes “market turning point.” A temporary rise becomes “confirmation.” A fall becomes “operator game.” A sideways market becomes “accumulation.”

The problem is not social media itself. Public discussion is healthy. Investors need information, debate, and access to opinions. But in Nepal’s market, online emotion often moves faster than verified information.

That creates a serious imbalance. Many retail investors see the narrative before they see the financial statement. They hear the slogan before they read the company report. They follow price movement before they understand the business. And once a story becomes popular enough, the story itself starts moving the market.

This is why NEPSE’s biggest weakness may not be volatility. It may be the quality of the conversation around volatility.

The market is full of questions that are rarely asked with enough discipline. Did the company’s earnings improve? Is the stock expensive or cheap compared to its fundamentals? Is the rise broad-based or concentrated in a few scripts? Is turnover healthy or speculative? Are investors buying a business or chasing a crowd? Is policy really changing, or are people only expecting it to change?

Without those questions, the market becomes vulnerable to mood.

And mood is not a foundation.

The appointment of Dr. Gopal Prasad Bhatt as chairperson of the Securities Board of Nepal has naturally become part of the current market conversation. SEBON is not a symbolic institution. It is the regulator responsible for the credibility of Nepal’s capital market. Its leadership matters for IPO approvals, market surveillance, broker regulation, disclosure discipline, investor protection, and overall trust. SEBON’s official website lists the newly appointed chairperson taking charge, along with recent capital-market notices and policy items.

So it is understandable that investors are watching the new leadership closely.

But expectation is not reform.

A new chairperson can create confidence. But confidence becomes meaningful only when it is followed by transparent decisions, consistent enforcement, stronger surveillance, better communication, and investor protection. Reform is not a headline. Reform is a system.

This distinction matters because NEPSE often reacts not only to what has happened, but to what investors think may happen. Investors price in possible changes to margin lending, IPO approvals, broker rules, liquidity conditions, and regulatory action. Sometimes those expectations are reasonable. Sometimes they are exaggerated. Sometimes the market moves first and waits for proof later.

That is risky.

If SEBON’s new leadership delivers credible reform, the market may gain a stronger foundation. But if investors price in hope before reform arrives, optimism becomes fragile. And fragile optimism can turn dangerous very quickly.

There is nothing wrong with optimism. Markets need optimism. Without the belief that the future can be better than the present, no one would invest.

But hype without foundation is catastrophic.

A market can rise because sellers are exhausted. It can rise because traders expect policy support. It can rise because liquidity improves. It can rise because a rumor spreads. It can rise because a few large players move first and the crowd follows. None of these reasons automatically proves that the real economy has improved.

That is the mistake many investors make.

They see movement and assume meaning.

A healthy market should rise because capital believes in future earnings, productive growth, and policy stability. But a fragile market can rise simply because people want to believe the worst is over.

There is a difference.

This is where NEPSE’s real problem begins. The index has become more powerful as a symbol of hope than as a mirror of economic strength. For many people, NEPSE represents the possibility of wealth in a country where regular income often feels limited, business confidence is weak, and young people continue to leave for opportunity abroad.

That emotional weight is important. It explains why people care so deeply. But it also explains why the market is vulnerable. When a stock market becomes one of the few places where people feel they can change their financial future, hope becomes easy to exploit.

The real problem NEPSE is facing is that it has grown as a trading obsession faster than Nepal has grown as a productive economy.

A stock market should help channel savings into productive companies. It should allow businesses to raise capital, give investors ownership in growth, and create a transparent system for valuing risk. At its best, a capital market connects ordinary savings with national development.

But when the market becomes dominated by short-term sentiment, rumor cycles, policy anticipation, and social media psychology, it begins to lose that purpose. It becomes less about capital formation and more about timing. Less about ownership and more about exit. Less about businesses and more about screens.

Nepal’s market structure itself shows why investors should be careful about treating NEPSE as a complete mirror of the national economy. Nepal Rastra Bank’s ten-month macroeconomic update for FY 2025/26 shows that banks, financial institutions, and insurance companies accounted for 50.7 percent of stock market capitalization in mid-May 2026, while hydropower companies accounted for 17.5 percent. In other words, NEPSE is heavily shaped by a few sectors; it does not perfectly represent the whole economy.

This matters. If investors watch only the index, they may miss the economy behind it. A movement in NEPSE is not the same as a movement in Nepal’s overall productive capacity. A banking-heavy and hydropower-heavy market can move for reasons that do not reflect the condition of agriculture, manufacturing, employment, small businesses, tourism, or household income.

That is why a green NEPSE should not automatically be read as a healthy Nepal.

There is a darker reality in NEPSE that many people talk about privately but few discuss openly.

The market may, at times, function as a wealth-transfer machine from uninformed late entrants to better-informed early movers.

This does not require accusing any specific person, broker, company, or group. It is a structural concern. In every market, information has value. People with better access, better timing, deeper networks, and stronger understanding of liquidity have an advantage. Those who enter late, after the story has already spread online, often carry the highest risk.

The darkest question in NEPSE is not why prices rise.

It is who gets to exit when the crowd finally enters.

This question matters because the market often speaks in the language of opportunity while hiding the mechanics of risk. When prices rise, everyone talks about confidence. When prices fall, losses become personal. The early mover may already be out. The promoter may already have benefited. The influencer may not bear any responsibility. The ordinary investor is left holding the lesson.

Many retail investors do not lose money because they are foolish. They lose because they are late. They lose because they are surrounded by noise. They lose because they confuse confidence with knowledge. They lose because the market rewards speed, access, and discipline more than emotion.

That is why regulation matters. That is why disclosure matters. That is why investor education matters. A market cannot be fair if some participants are trading information while others are trading hope.

The most uncomfortable question in Nepal’s stock market debate is also the simplest one:

Is Nepal’s real economy strong enough to justify the optimism being priced into NEPSE?

A stock market can rise while the economy weakens. That can happen. Markets are forward-looking. They may price in future reform, better liquidity, lower interest rates, or sector-specific expectations. But if the gap between market optimism and economic reality becomes too wide, the market starts pricing an illusion.

Nepal’s economic outlook deserves more attention than it receives in daily market conversations. The World Bank projected Nepal’s growth to slow to 2.3 percent in FY26 from 4.6 percent in FY25, citing the impact of the Middle East conflict and the lingering effects of domestic disruptions. It also said the slowdown is expected to be concentrated in services, with tourism, transport, domestic trade, and real estate activity facing pressure.

That does not mean Nepal is in a depression. That word should be used carefully. But it does mean the economy is under pressure. A slowdown of that scale should make investors ask harder questions about company earnings, consumer demand, bank credit, tourism, government spending, and business confidence.

If the real economy is slowing, why does the market become so quick to celebrate?

That is not a rhetorical question. It is the heart of the article.

The problem is not that investors are hopeful. The problem is that hope often moves faster than economic evidence.

Nepal’s latest budget has added another layer to this conversation.

A large budget can create confidence. It can suggest ambition, spending, development, and state support. But budget size alone means very little. The real question is how the money will be raised, how much will actually be spent, and whether that spending will create future productivity.

For FY 2026/27, the government announced a budget of Rs 2,124.34 billion. The financing plan includes revenue, foreign grants, foreign loans, and domestic borrowing. According to The Rising Nepal, the budget targets Rs 1,405.31 billion in revenue, with the remaining resources to be covered through Rs 61.74 billion in foreign grants, Rs 247.28 billion in foreign loans, and Rs 410 billion from domestic borrowing.

The important point is not simply the headline size of the budget. The important point is that a major part of the spending plan depends on borrowing.

Debt is not automatically bad. Countries borrow to build roads, hydropower, transmission lines, schools, hospitals, and productive infrastructure. Borrowing becomes dangerous when it does not create returns.

That is the question Nepal must answer.

Is public borrowing creating future productive capacity, or is it increasingly being used to manage present pressure?

This matters for NEPSE because the market cannot be separated from public finance. If debt servicing grows, if revenue remains weak, if capital expenditure is poorly executed, and if domestic borrowing tightens financial space, the effects eventually reach banks, companies, consumers, and investors.

Nepal’s outstanding public debt has moved close to Rs 3 trillion. Kantipur reported that outstanding public debt had reached Rs 2,975.4 billion as of Baisakh, equal to 45.08 percent of GDP. The Kathmandu Post separately reported, citing the Public Debt Management Office, that public debt increased by Rs 300.99 billion during the first ten months of the fiscal year.

A market can ignore debt for a while.

An economy cannot.

Another dangerous illusion is that NEPSE exists inside Nepal alone.

It does not.

Nepal imports global shocks through fuel prices, remittances, tourism, imports, exchange rates, foreign debt, migration destinations, and investor confidence. A conflict in the Middle East is not just foreign news for Nepal. It can affect oil prices, transport costs, remittance flows, tourist arrivals, inflation, and the burden of external debt.

The World Bank’s June 2026 Global Economic Prospects forecast global growth to slow to 2.5 percent in 2026 from 2.9 percent in 2025, with risks linked to conflict, energy prices, inflation pressure, commodity disruptions, and policy uncertainty.

That matters for Nepal. A remittance-dependent, import-dependent, tourism-sensitive economy cannot treat global weakness as background noise. If external conditions worsen, Nepal feels it through households, businesses, banks, government revenue, and eventually the stock market.

Yet most NEPSE discussions remain too domestic. Investors talk about SEBON, NRB, brokers, margin lending, IPO approvals, and budget provisions. Those things matter. But they are not the whole story.

Nepal is not an island.

And neither is NEPSE.

Nepal does have important buffers. Nepal Rastra Bank’s ten-month macroeconomic update shows gross foreign exchange reserves rising to Rs 3,704.55 billion by mid-May 2026, enough to cover 22.6 months of prospective merchandise imports and 19.2 months of merchandise-and-services imports. Remittance inflows also increased 41.2 percent to Rs 1,916.90 billion during the first ten months of FY 2025/26.

That matters. Strong reserves give policymakers breathing space. Remittances support households, consumption, and the external sector. Nepal is not facing an immediate external crisis in the way some pessimistic narratives may suggest.

But reserves do not solve everything.

A country can have comfortable reserves and still struggle with weak productivity. It can receive remittances and still fail to create enough domestic jobs. It can have macro stability and still face poor capital spending, weak private investment, low industrial growth, and rising fiscal pressure.

Reserves buy time.

They do not automatically build an economy.

That is why NEPSE optimism must be judged carefully. Nepal has buffers, yes. But it also has structural weaknesses. The danger is when investors see only the comfort and ignore the cracks.

Amid all the talk about NEPSE, Nepal may be forgetting a basic truth: a stock market does not create wealth simply by going up.

Real wealth comes from production. It comes from businesses that earn, hydropower projects that generate returns, hotels that bring tourists, factories that sell goods, technology firms that scale, farms that become productive, infrastructure that lowers costs, and institutions that make investment trustworthy.

NEPSE should help finance that process.

But if the market becomes mostly a place for short-term speculation, it stops serving its deeper purpose. It becomes a space where people chase price movement instead of ownership, narratives instead of earnings, and timing instead of value.

That is not a mature capital market.

A mature capital market does not only ask, “Which stock will rise?”

It asks,

Until those questions become central, NEPSE will remain vulnerable to illusion.

The answer is not to attack NEPSE. Nepal needs a stronger capital market, not a weaker one. The market can mobilize savings, finance companies, support entrepreneurship, and give ordinary citizens a stake in economic growth.

But for that to happen, reform must mean more than making the index rise.

For SEBON, reform should mean stronger surveillance, faster enforcement, clearer IPO standards, transparent communication, action against misinformation, and a market where ordinary investors feel protected without being misled.

For NEPSE, reform should mean better data access, stronger technology, clearer market information, improved transparency, and tools that allow investors to understand movements instead of only reacting to them.

For the government and NRB, reform should mean stable policy, credible budgeting, debt discipline, productive capital spending, and clarity around liquidity and margin-related rules.

For listed companies, reform should mean better reporting, honest project updates, stronger governance, and respect for shareholders.

For investors, reform should mean discipline. It means reading financial statements. It means understanding debt. It means asking whether a company earns enough to justify its price. It means knowing the difference between trading and investing. It means refusing to buy simply because the screen is green.

NEPSE does not need blind confidence. It needs mature confidence.

A green screen is not enough. A bigger budget is not enough. A new regulator is not enough. Social media optimism is not enough.

That is the difference between a market that grows and a market that traps.

The danger facing NEPSE is not investor hope. Hope is necessary in every market. The danger begins when hope replaces evidence.

Nepal’s stock market has the potential to become a stronger institution. It can channel savings into productive investment, reward disciplined investors, and support national economic development. But that potential will remain limited if the market stays trapped in a cycle of rumor, hype, policy expectation, and emotional trading.

A rising index can signal confidence, but it cannot prove strength on its own. A new regulator can create expectation, but not reform by itself. A large budget can suggest ambition, but not guarantee productivity. Strong reserves can provide comfort, but not solve structural weakness. A viral market narrative can create excitement, but not economic value.

The real question is whether Nepal is building the economic foundation needed to justify market optimism.

Until that question is answered, every green screen should be read with caution — not fear, but caution.

Because the most dangerous illusion in NEPSE is not that the market may fall. It is that too many investors may believe it is strong simply because, for a moment, it is green.